Trillions of dollars in crypto liquidity is concentrating inside the venues US regulators fear most

Crypto market liquidity is more and more hyper-concentrating inside a handful of large buying and selling venues, making a market construction that international central financial institution researchers warn is evolving right into a closely leveraged “shadow crypto monetary system.”

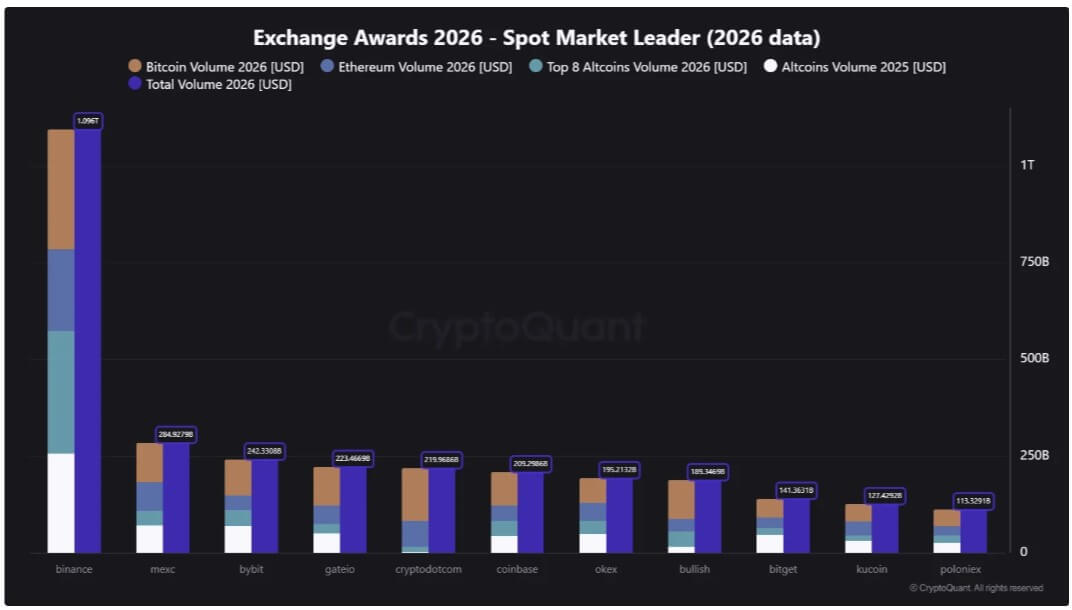

Data from CryptoQuant exhibits that Binance, the world’s largest crypto trade, cleared over $1 trillion in buying and selling quantity through the first 112 days of 2026.

That is considerably increased than the overall of rival platforms like MEXC, which stood at about $284.9 billion; Bybit at $242.3 billion; Crypto.com at $219.9 billion; Coinbase at $209.3 billion; and OKX at $195.2 billion.

The hole provides a market anchor to a brand new Monetary Stability Institute paper printed by the Financial institution for Worldwide Settlements, which mentioned massive crypto platforms have expanded past buying and selling and custody into yield merchandise, lending, derivatives, staking, and token-related providers.

The paper described many of those buying and selling platforms as “multifunction cryptoasset intermediaries” (MCIs) as a result of they now mix roles which are often break up amongst banks, brokers, exchanges, and custodians in conventional finance.

Attributable to this, BIS flagged issues that the crypto buying and selling venues attracting the deepest liquidity are additionally turning into the locations the place customers retailer belongings, put up collateral, take leverage, and search yield.

That has turned the present trade focus right into a wider query for regulators: whether or not platforms constructed for crypto buying and selling have turn into monetary intermediaries earlier than the principles round buyer belongings, leverage, and liquidity danger have caught up.

Liquidity is concentrated the place danger is rising

Crypto’s buying and selling base has not unfold evenly throughout a whole bunch of platforms regardless of years of trade failures, enforcement actions, and market drawdowns.

The BIS paper mentioned there have been about 200 to 250 energetic centralized spot exchanges as of 2025, however buying and selling remained dominated by a small group of enormous platforms.

BIS identified that Binance accounted for about 39% of world centralized trade spot quantity, whereas the highest 10 exchanges dealt with about 90% of world buying and selling exercise.

The BIS paper mentioned the biggest MCIs typically function by subsidiaries or licensed entities throughout greater than 100 jurisdictions. It additionally cited estimates that the highest 5 MCIs collectively serve about 200 million to 230 million distinctive customers, with 20 million to 34 million utilizing staking or earn merchandise.

Which means the most important crypto exchanges are now not simply locations the place patrons meet sellers. They’re turning into balance-sheet hubs for a market that also lacks lots of the authorized protections constructed into conventional finance.

That construction provides the biggest venues energy past extraordinary market share as their order books affect pricing and their derivatives merchandise form leverage.

On the identical time, their custody programs maintain the belongings clients use to maneuver throughout spot, margin, staking, and yield merchandise.

Binance’s $1.09 trillion in early-year quantity exhibits the drive of that community impact. Merchants proceed to cluster the place liquidity is deepest and execution is most dependable.

In regular circumstances, that focus can cut back friction. Throughout stress, it will possibly make a handful of venues central to the best way losses transfer by the system.

Exchanges have gotten monetary supermarkets

The enterprise mannequin that has made massive exchanges commercially highly effective is identical mannequin now drawing scrutiny.

A serious crypto platform can provide spot buying and selling, perpetual futures, custody, staking, lending, secured borrowing, pockets providers, and yield merchandise below one roof. Some additionally function affiliated token ecosystems or infrastructure tied to their broader platforms.

In conventional finance, these providers are often break up amongst establishments with completely different capital, liquidity, disclosure, and conduct guidelines. Banks, brokerages, exchanges, clearinghouses, and custodians every sit inside particular regulatory lanes.

Crypto has moved towards a extra built-in mannequin. A consumer can deposit belongings, commerce spot tokens, borrow in opposition to collateral, open leveraged derivatives positions, and allocate idle balances to yield merchandise with out leaving the platform.

That mannequin retains capital contained in the venue. Nonetheless, it additionally makes it tougher for customers and regulators to separate buying and selling danger from credit score, custody, and liquidity dangers.

The BIS paper mentioned MCIs that settle for buyer belongings by funding packages and use them for lending, market-making, or different actions tackle dangers much like these confronted by monetary intermediaries. These embody credit score danger, maturity danger, and liquidity danger.

The distinction is that many crypto platforms don’t face the identical prudential necessities as banks or regulated broker-dealers. They will not be topic to comparable capital buffers, liquidity guidelines, deposit safety, stress exams, or decision frameworks.

Yield turns balances into credit score publicity

The clearest instance is the expansion of earn-and-yield merchandise.

These merchandise are sometimes marketed as a means for customers to earn passive returns on idle crypto belongings.

Nonetheless, the financial actuality could be a lot much less easy. Relying on the phrases, clients could give the platform management over their belongings, permitting these funds for use for staking, lending, market-making, margin financing, or different actions.

The BIS paper mentioned some preparations can go away clients with an unsecured declare on the middleman slightly than a protected proper to particular belongings. In observe, the consumer could consider the product as a financial savings account, whereas the authorized publicity resembles a mortgage to the platform.

That distinction turns into essential in a disaster.

A financial institution depositor is often protected by a framework constructed round capital necessities, liquidity administration, deposit insurance coverage, and entry to central financial institution liquidity in excessive instances.

A crypto trade buyer utilizing a yield product could have none of these protections. If the platform can not meet withdrawals or suffers buying and selling losses, the client could turn into an unsecured creditor.

The BIS cited Celsius Community and FTX’s chapter as examples of how these weaknesses can floor.

Celsius supplied yield merchandise that trusted lending, leverage, and liquidity transformation. When market circumstances turned, and clients sought withdrawals, the platform failed.

However, FTX uncovered a distinct model of the identical structural drawback, with buyer belongings, affiliated buying and selling exercise, and group-level danger turning into entangled.

These examples stay essential as a result of the biggest exchanges at the moment are larger, extra international, and extra embedded in crypto market infrastructure than many failed corporations have been in 2022.

Leverage can transmit stress quick

The BIS warning additionally extends past buyer safety into market construction.

Crypto derivatives markets run repeatedly, use automated liquidation engines, and sometimes depend on collateral whose worth can fall sharply inside minutes. When leverage is targeting the identical venues that dominate spot liquidity, value shocks can turn into liquidation occasions earlier than human merchants have time to reply.

The BIS pointed to the October 2025 flash crash for example of how briskly the system can transfer. The episode triggered about $19 billion in pressured liquidations throughout crypto derivatives markets and affected greater than 1.6 million merchants.

The crash confirmed how tightly related leverage, collateral, automated danger engines, and venue focus have turn into. Notably, some market observers blamed the October 10 incident on Binance’s working practices.

It’s because a pointy macro transfer hit spot costs, leading to a value decline that weakened collateral. Then, this weaker collateral triggered margin calls, which pressured liquidations and deepened the downward value transfer.

That loop is just not distinctive to crypto, however the rising market construction can speed up it.

Giant exchanges sit on the heart of that course of as a result of they host the liquidity, collateral accounts, and derivatives positions by which deleveraging happens. A short outage, pricing hole, or liquidity shortfall at a dominant venue can have an effect on greater than that venue’s personal customers. It may well affect market costs throughout the sector.

Regulators face a enterprise mannequin that outgrew the trade label

In opposition to this backdrop, the coverage problem is that the biggest crypto platforms don’t match neatly into current classes.

A single agency could function as an trade, custodian, dealer, lender, staking supplier, derivatives venue, and pockets infrastructure supplier concurrently. Every exercise could fall below a distinct regulator, or outdoors clear oversight altogether, relying on the jurisdiction.

Consequently, the BIS paper known as for prudential necessities for MCIs engaged in monetary intermediation. These may embody capital and liquidity buffers, stronger governance requirements, stress testing, risk-management guidelines, and clearer segregation of buyer belongings.

It additionally urged that regulators might have each entity-based and activity-based guidelines. Entity-based guidelines would take a look at the well being and construction of the platform as an entire. Exercise-based guidelines would apply to particular providers akin to lending, custody, staking, derivatives, or yield merchandise.

That method would mark a shift from treating massive crypto corporations primarily as buying and selling platforms to extra carefully aligning them with their surrounding monetary conglomerates.

This could now elevate questions on how they handle balance-sheet danger, shield buyer belongings, deal with liquidity stress, and the way a failure could be contained.

In the meantime, this concern is turning into extra pressing as conventional finance hyperlinks to crypto deepen by exchange-traded merchandise, institutional custody, stablecoin reserves, and brokerage integrations.

The BIS paper warned that as MCIs turn into extra related to conventional finance, disruptions at main platforms may have penalties past the crypto ecosystem.