Where to Draw the Legal Line?

In March 2023, the SEC charged eight celebrities with violating sure provisions of the Securities Act of 1933 of their promotion of cryptocurrency belongings. The costs stem from Part 17(b) of the act, an anti-fraud and anti-touting provision that addresses the failure to reveal funds associated to promotional exercise.

The group of celebrities — which included Lindsay Lohan, Jake Paul, and Ne-Yo —particularly confronted accusations of illegally selling Tron (TRX) and/or BitTorrent (BTT) tokens supplied by corporations underneath the route of Tron founder Justin Solar.

Whereas the SEC gained the case, the questions on the coronary heart of the matter stay unanswered: The place does praising a cryptocurrency finish and selling one start? Can there be such a factor as reputable cryptocurrency promotion? And what determines the standing of the asset as a safety?

Different ongoing authorized battles associated to the unlawful promotion of crypto — together with these involving celebrities endorsing FTX like Tom Brady, Larry David, Stephen Curry, and others — revolve across the identical essential questions. With more than 20 percent of U.S. shoppers proudly owning and utilizing crypto, it’s evident that clear strains have to be drawn when promoting and selling digital belongings.

So, the place is that line? And is there a authorized distinction between merely supporting a selected digital asset and unlawfully selling it?

“Affordable client/investor” vs. public determine/superstar

On the most foundational stage, the primary query that needs to be requested is how we outline what it means to “patronize” and assist a specific digital asset — the place a person is merely sharing their funding holding with household, mates, and colleagues —versus what it means to “promote” that specific digital asset to a community-at-large with the particular intent of persuading one other to take a position their cash into that particular person asset.

Patronizing a digital asset isn’t too totally different from an individual merely sharing what shares they personal with a member of the family, good friend, or colleague. On this case, now we have to imagine that the common client doesn’t totally perceive the mechanics of cryptocurrency, the way it works, and the legal guidelines surrounding it — particularly for the reason that legal guidelines and rules surrounding it are virtually non-existent on the subject of the sale and promotion of digital belongings.

So, what’s “tipping” the size of a person harmlessly sharing pleasure a couple of explicit digital asset to taking a considerable step in eager to create an “financial reliance” of such a magnitude that crosses into SEC territory?

It might appear that the particular details and circumstances of the promotion that’s predicated upon the next:

(1) who you might be as an individual/firm,

(2) the assets at your disposal to deliberately talk and promote the asset,

(3) the probability that your message/promotion will attain a big neighborhood of individuals, and

(4) the probability that the message/promotion will closely affect a 3rd celebration’s choice in order to create an financial reliance and monetary choice based mostly upon your social standing.

Addressing the primary ingredient of “who the promoter is,” it could make sense to use a “Affordable Individual” commonplace, which might draw the road of whether or not we’re speaking about an on a regular basis client (skilled or novice) or a public determine/superstar, which carries further weight and obligations.

Normally, it could seem {that a} cheap, common client who’s supporting and sharing their funding into a specific digital asset is (usually) not going doing it for the expectation of serving to improve the ground worth or market worth of that specific asset.

#TRX 🚀 @justinsuntron https://t.co/xh6xB6fNmo

— Jake Paul (@jakepaul) February 13, 2021

A public determine or superstar, however, has by and thru their “public” standing a uniquely highly effective skill to speak at giant a message or concept that has a really sturdy probability of persuading huge quantities of individuals to behave or behave in a sure means – no matter how skilled or well-versed they’re in with the ability to convey such a message precisely.

Because of this, figuring out who is definitely selling the digital asset is essential in assessing the “why” behind their promotion and whether or not it constitutes an “unlawful promotion” underneath present securities regulation.

The “feel and look” of the promotion

One other necessary facet of figuring out the distinction between patronizing and selling is the “feel and look” of what’s being shared. We’ve seen the SEC come down onerous on superstar endorsements of digital belongings that finally converse to the appear and feel of the superstar’s promotion of a cryptocurrency, together with the verbiage and nature of the disclosures particularly expressed within the submit.

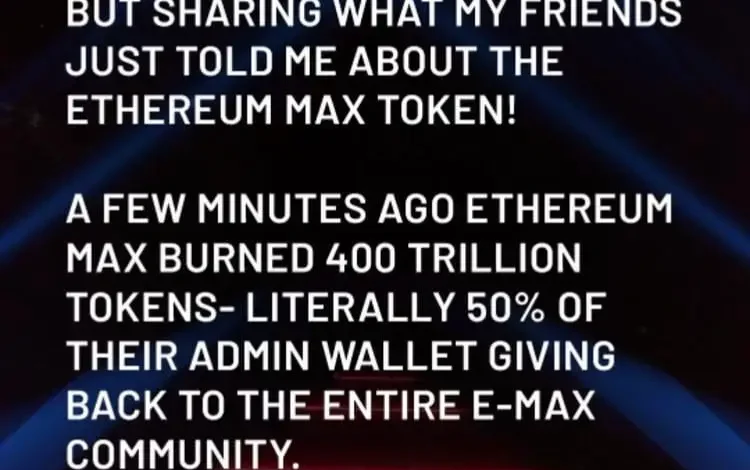

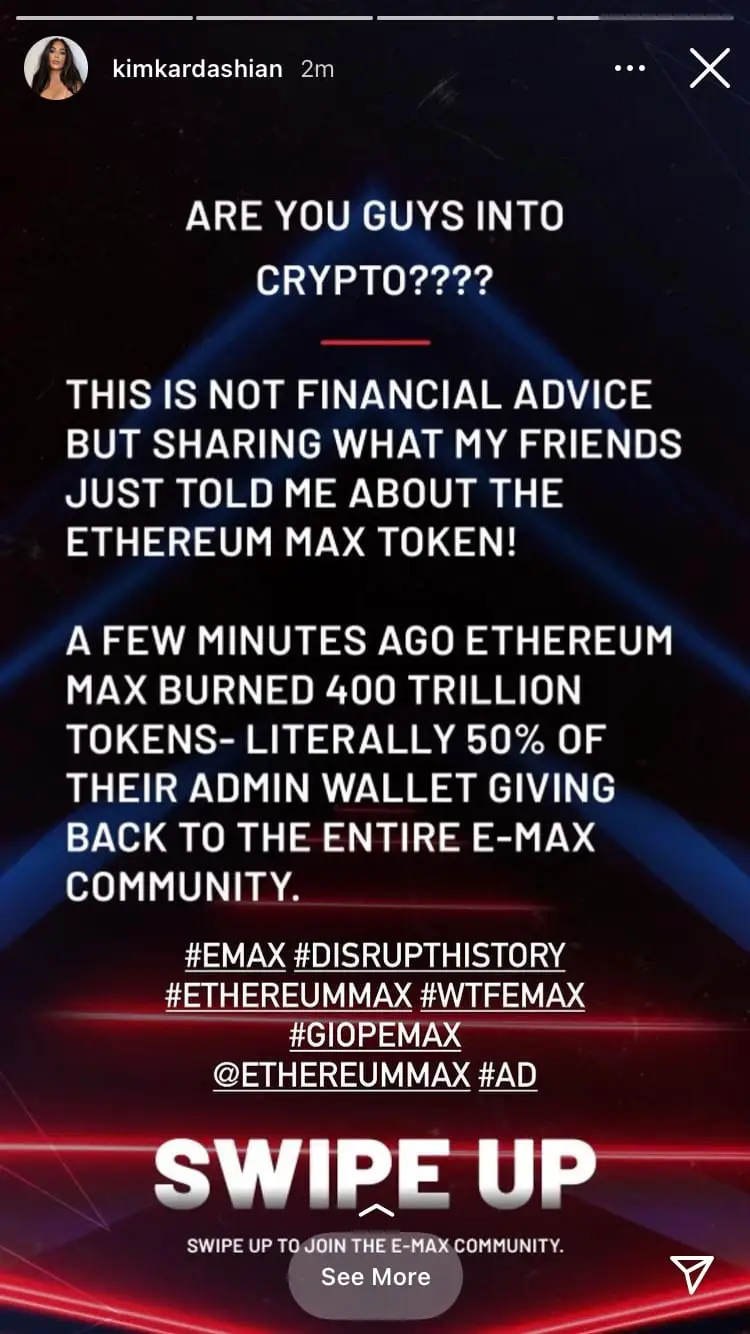

This started in October 2022 with Kim Kardashian and her unlawful promotion of EthereumMax (EMAX).

Whereas Kardashian agreed to settle the fees, paying $1.26 million in penalties, disgorgement, and curiosity, the SEC discovered that Kardashian had didn’t disclose that she was paid $250,000 to publish a submit in 2021 on her Instagram account (which now has 359M followers) about EMAX tokens.

Her submit contained a hyperlink to the EthereumMax web site, which offered directions for potential traders to buy EMAX tokens, however nothing else. Whereas Kardashian had said in her submit that it was “not monetary recommendation” along with including totally different hashtags together with “#advert,” the SEC stated that wasn’t sufficient for compliance.

Different celebrities focused by the SEC included Floyd Mayweather, Jr., DJ Khaled, Lindsay Lohan, Jake Paul, Soulja Boy, Akon, Ne-Yo, and Lil Yachty for a similar causes.

thanks guys, purchased some BNB, DGB, TRX, KLV, ZPAE and FDO 💪🏾 what’s subsequent? let’s go ✔️

— Soulja Boy (Draco) (@souljaboy) January 22, 2021

Then, in November 2022, FTX declared chapter, resulting in the collapse of the alternate and one of many greatest monetary scandals since Enron and Bernie Madoff.

From Tom Brady, Madonna, and Gwyneth Paltrow to David Ortiz, Larry David, Jimmy Fallon, and extra, the SEC introduced its costs as FTX’s collapse continued to unwind whereas additionally showcasing the necessity for public figures to make the right disclosures on their social media posts and TV commercials that they’re getting paid to advertise these digital belongings.

This was a reminder and warning to celebrities and different public figures that they can’t escape the necessities of the anti-touting provision of Part 17(b) of the Securities Act of 1933, which requires them to open up to the general public when they’re getting paid to advertise one thing, how a lot they’re getting paid to advertise investing in securities.

Underneath Part 17(b), a “promoter” is prohibited from publishing or circulating an article or communication for ‘a consideration acquired’ with out totally disclosing that consideration. Underneath the regulation, a “consideration” is a mutual alternate of worth that helps solidify the enforcement of a authorized contract or settlement.

Navigating the unknown

Sadly, there’s nonetheless a grey space in regards to the anti-touting provisions of Part 17(b), as a result of it solely applies if the instrument being promoted is a “safety.” And we nonetheless don’t have clear steerage on what constitutes a “safety.”

This brings us to the latest sudden crackdown by the SEC towards two of the world’s greatest crypto exchanges and the continuing debate and controversy surrounding the SEC’s “enforcement by regulation” method that’s drastically harming the expansion and growth of the {industry}.

Senator Cynthia Lummis (R-WY), who, along with Senator Kirsten Gillibrand (D-NY), has been a powerful advocate for the institution of a whole regulatory framework, took to Twitter to share her adamant belief that the SEC has “failed to supply satisfactory authorized steerage on what differentiates a safety from a commodity.”

My assertion on the SEC suing Coinbase, inc. https://t.co/5KNEM0IPSV pic.twitter.com/EgRIxrIcjj

— Senator Cynthia Lummis (@SenLummis) June 6, 2023

Each she and Senator Kirsten Gillibrand (D-NY) have been the driving power behind their proposed, landmark bipartisan laws – the Responsible Financial Innovation Act, that may create a whole regulatory framework for digital belongings that encourages accountable monetary innovation, flexibility, transparency, and sturdy client protections whereas integrating digital belongings into present regulation – resembling Howey.

The landmark 1946 U.S. Supreme Courtroom case of Howey is the center of any conventional securities evaluation, presenting components that have to be thought of in serving to decide whether or not an instrument is taken into account a “safety” or “funding contract.”

An industry-wide gray space

Because it stands, this {industry} is working within the grey by way of how they introduce a digital asset to its buyer base and the mechanisms underlying its buy and sale of them, together with the strategies they use to advertise and/or in any other case promote the asset providing.

The pending litigation that we’re watching unfold will unquestionably carry these circumstances entrance and heart, starting with what standards makes a digital asset or providing a “safety” (versus a commodity) and the way an organization or model is ready to legitimately promote that asset or providing to traders and most of the people with out violating securities regulation.

The knowledge offered on this article doesn’t, and isn’t supposed to, represent authorized recommendation; as an alternative, all info, content material, and supplies obtainable on this web site are for common informational functions solely. Data on this web site could not represent probably the most up-to-date authorized or different info. This web site comprises hyperlinks to different third-party web sites. Readers of this text ought to contact their lawyer to acquire recommendation with respect to any explicit authorized matter. No reader, person, or browser of this web site ought to act or chorus from appearing on the premise of knowledge on this web site with out first in search of authorized recommendation from counsel within the related jurisdiction.