The SEC looks at a 1990s fix for crypto markets to allow true “innovation pathway”

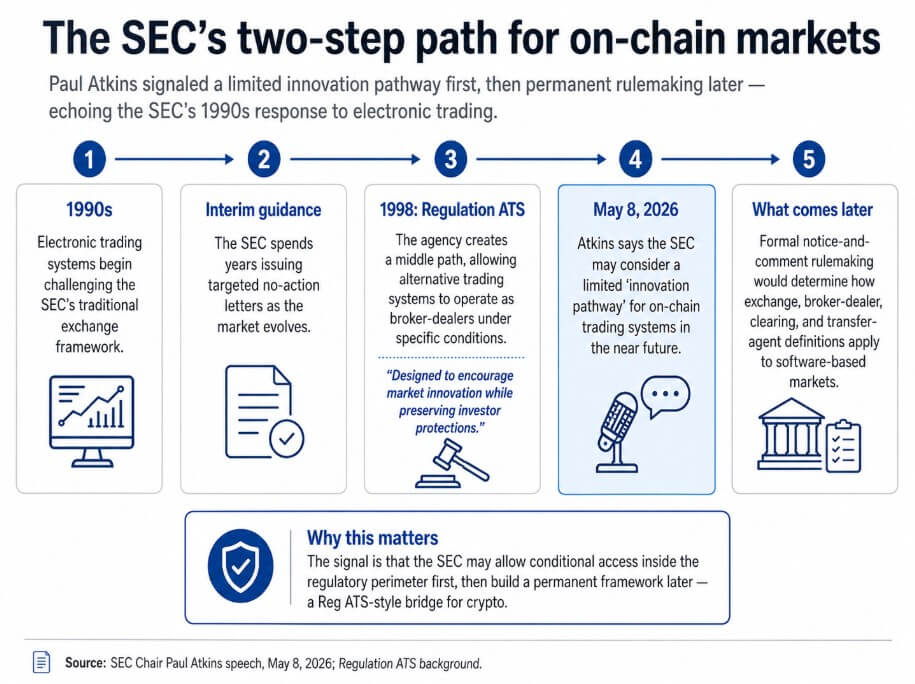

In a Might 8 speech, SEC Chair Paul Atkins stated the company may take into account a restricted “innovation pathway” for on-chain buying and selling programs within the close to future.

In the meantime, the company will reserve formal notice-and-comment rulemaking to find out how crypto platforms match contained in the change definition. Atkins tied that concept on to the SEC’s dealing with of digital buying and selling within the Nineties.

The SEC spent years issuing advert hoc no-action letters as digital buying and selling challenged the change framework, then constructed Regulation ATS in 1998. The rule was a center path that allowed various buying and selling programs to function as broker-dealers beneath particular situations because the market matured.

The unique adopting launch described the framework as designed to “encourage market innovation” whereas preserving investor protections. Atkins is pointing at that sequence of focused steerage first, fit-for-purpose structure second, as a template for on-chain finance.

The 2-step studying makes the speech totally different from generic crypto-policy rhetoric.

Atkins appears to be preparing the SEC to permit sure on-chain buying and selling programs to function contained in the regulatory perimeter beneath situations, whereas an extended rulemaking course of settles how change, broker-dealer, clearing, and transfer-agent definitions apply to software-based markets.

For crypto companies that spent years dealing with enforcement earlier than guidelines existed, that sequence would signify a real departure from current company posture.

Why on-chain markets drive a brand new structure

Conventional SEC guidelines have been constructed round separate actors performing separate regulated features, equivalent to exchanges matching orders, broker-dealers routing and executing them, clearing companies settling them, and switch brokers recording possession.

A single on-chain protocol can carry out all of these features mechanically, typically inside seconds, with out distinct intermediaries at every step.

Making use of a rulebook designed for that separation to software program that collapses it produces authorized uncertainty that companies and regulators alike try to flee, and Atkins acknowledged that friction immediately.

Clear compliance requires the SEC to do greater than declare present guidelines apply. Some features that seem like change exercise in on-chain kind additionally resemble broker-dealer or clearing exercise, or each concurrently.

A restricted pathway is meant to handle this downside by giving companies a path to function contained in the perimeter earlier than the harder definitional rewrites are full.

| Conventional SEC class | Conventional perform | What an on-chain protocol can do |

|---|---|---|

| Trade | Matches purchase and promote orders | Executes trades mechanically throughout the protocol |

| Dealer-dealer | Routes and executes buyer orders | Routes liquidity and executes transactions by software program |

| Clearing company | Clears and settles trades between events | Settles transactions on-chain, typically inside seconds |

| Switch agent | Maintains data of possession | Updates possession data immediately on-chain |

This pathway may take the type of exemptive reduction, conditional no-action letters, a pilot program, a tailor-made registration framework, or a registration-lite mannequin for sure on-chain venues.

The sequence is near-term conditional entry, then formal rulemaking to future-proof the framework.

The SEC has already been working with momentary instruments on this area. On Apr. 13, the Division of Buying and selling and Markets issued a employees assertion providing conditional reduction to sure self-custodial crypto interfaces, calling it an “interim step” whereas broader regulatory questions are thought of.

Between Mar. 17 and Might 4, the SEC’s Crypto@SEC web page recorded 5 market construction or tokenization actions, and Atkins’ speech serves because the coverage body that connects these operational strikes right into a coherent sequence.

Commissioner Hester Peirce pointed to particular design levers in December 2025, asking whether or not the SEC ought to tailor Kind ATS for crypto various buying and selling programs, revise public-versus-non-public disclosure necessities, and rethink ATS reporting in gentle of public blockchains.

The February FAQ clarified that pairs buying and selling of securities and non-security crypto property is permissible, confirmed that present ATS kinds can accommodate crypto disclosures, and established that broker-dealer ATS operators might carry out sure clearing and settlement features beneath relevant legislation.

The pathway Atkins is hinting at seems to construct on these elements.

Bridge or funnel

The optimistic studying is that the SEC is making ready a real Reg ATS-style bridge, with formal conditional pathways for on-chain venues, purpose-built disclosure frameworks, and specific recognition that some on-chain clearing and settlement can sit inside broker-dealer exercise.

In that model, companies which have operated offshore or in authorized ambiguity would have a sensible path to register, disclose, and function domestically.

The Nasdaq tokenized-securities approval, the NYSE tokenized-securities submitting, and the HQLAx no-action reduction are all operational proof that the SEC can construction conditional lodging with out ready for Congress.

Conditional lodging and deregulation are distinct outcomes. The unique Regulation ATS introduced new buying and selling venues contained in the SEC’s perimeter and imposed situations on their operation.

A crypto equal would impose necessities on disclosure, recordkeeping, custody requirements, routing transparency, and conflict-of-interest controls, with a framework constructed round how on-chain protocols really perform.

The sensible profit to the trade could be a compliance route constructed on an on-chain structure.

The pessimistic studying is that the pathway materializes primarily for intermediated or hybrid actors, leaving autonomous protocols and decentralized programs in the identical authorized uncertainty they face in the present day.

The conditional reduction it presents applies solely to suppliers that maintain no buyer property, take no orders, route no transactions, execute no trades, and solicit no particular person exercise. That exclusion record covers most of what makes an automatic market-maker or lending protocol perform.

A pathway designed round these parameters would assist companies closest to the standard broker-dealer mannequin whereas doing little for elements of on-chain finance that don’t have any apparent broker-dealer analog.

| Optimistic studying | Pessimistic studying |

|---|---|

| Creates a workable compliance route for on-chain venues | Helps primarily hybrid or intermediated actors |

| Makes use of tailor-made disclosure and reporting necessities | Leaves autonomous protocols in authorized limbo |

| Brings exercise onshore as an alternative of pushing it offshore | Turns into a funnel into tighter SEC management |

| Offers the SEC visibility with out counting on enforcement first | Reduction is simply too slender to vary a lot in apply |

| Acknowledges that software-based markets don’t map neatly onto legacy change guidelines | Principally advantages companies closest to the broker-dealer mannequin |

Atkins additionally used the speech to induce Congress to ship the CLARITY Act to President Donald Trump’s desk, and the legislative backdrop helps clarify why SEC motion carries unbiased weight.

CLARITY Act confronted a February stalemate over stablecoin rewards provisions, an April push from Treasury Secretary Scott Bessent, and a Might 1 deal on a key provision which will restore Senate momentum.

That stop-start trajectory means the SEC should act with its personal instruments whereas Congress negotiates, and Atkins stated in January that statute alone leaves operational questions for the company to reply.

His FTX reference closed the political argument, noting that regulatory voids displace threat offshore, leaving American traders uncovered.

FTX operated outdoors the US, but American prospects nonetheless misplaced cash. A home pathway brings exercise contained in the system earlier than the subsequent structural failure makes the gaps simple.

The speech is finest taken as a marker that the SEC seems to be transferring from a classification argument about crypto becoming the previous rulebook to a design train about what situations a bridge for on-chain venues would really require.