Singapore puts Hyperliquid on warning list over protections it says it never claimed

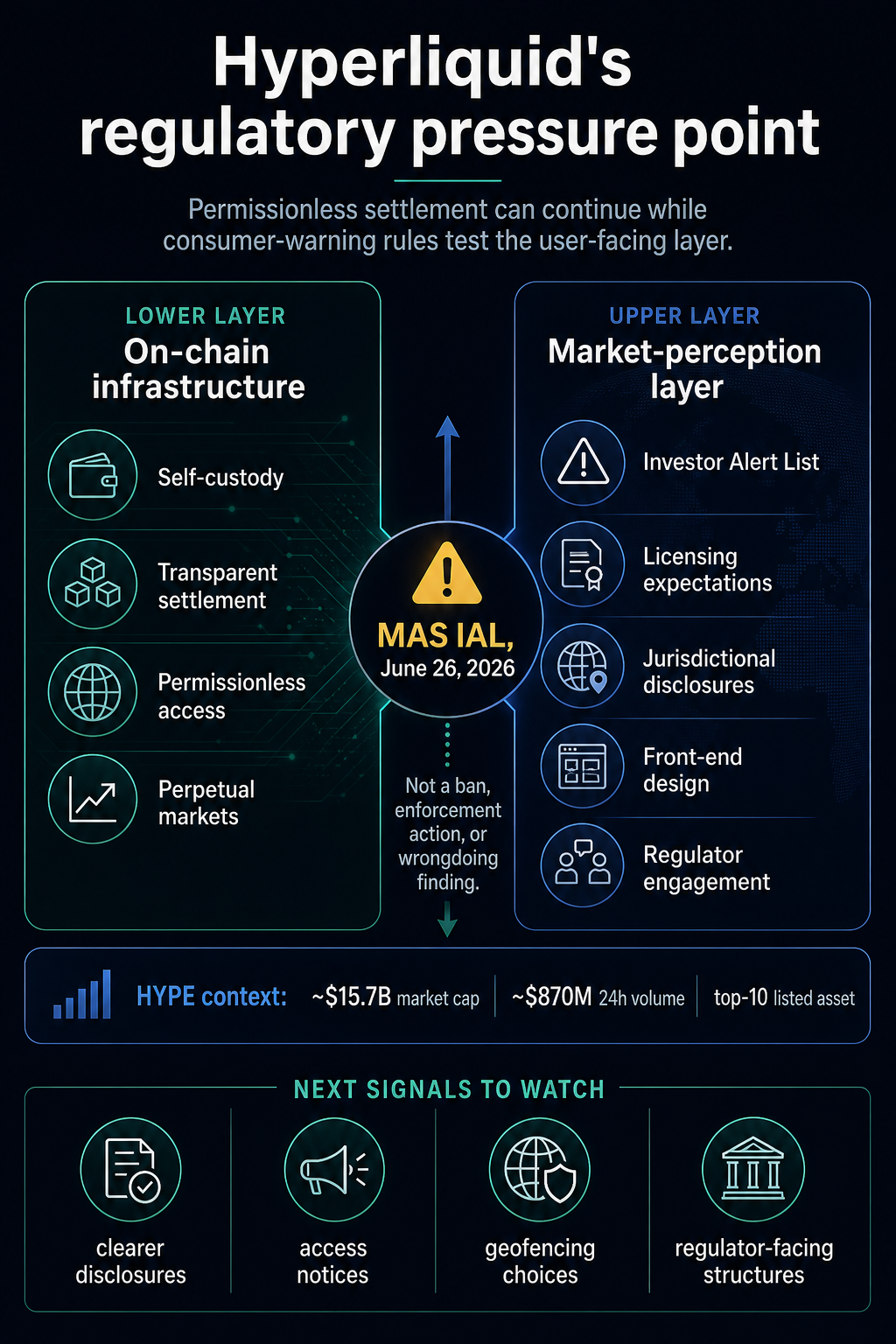

Hyperliquid has been added to Singapore’s Investor Alert List, placing DeFi’s permissionless pitch to a consumer-protection take a look at: the community can maintain settling trades, whereas the interface and public messaging round it draw regulatory scrutiny.

Hyperliquid stated in a June 26 statement that its look on the Financial Authority of Singapore’s listing was a warning-list occasion moderately than a ban, enforcement motion, or discovering of wrongdoing.

The venture additionally stated it had not claimed to be licensed by MAS, described itself as permissionless infrastructure, and stated customers retain self-custody whereas transactions settle transparently on-chain.

The ensuing stress is utilized to the user-facing layer. A high-performance on-chain derivatives venue can maintain processing trades and nonetheless face questions on whether or not its interface, documentation, and public messaging lead retail customers to imagine they’re accessing a regulated market.

Singapore’s alert, subsequently, now strikes the regulatory take a look at towards client notion.

The warning listing assessments the market-facing edge

MAS’s Investor Alert Listing is a public warning software. Singapore’s public supplies body the listing round unregulated individuals or entities which may be wrongly perceived as licensed or licensed by MAS.

MoneySense, Singapore’s nationwide monetary schooling program, warns that buyers who cope with unregulated individuals might forgo the protections out there beneath MAS rules, and that the listing isn’t exhaustive.

That consumer-protection framing sits aside from any discovering that Hyperliquid broke Singapore legislation. MAS stated when it launched the IAL in 2004 that publishing a reputation on the listing didn’t imply the authority had concluded that the particular person had contravened the legislation.

Hyperliquid’s personal response leans on the identical boundary. The venue’s assertion says the itemizing doesn’t quantity to a ban or enforcement discovering, whereas additionally stressing that customers don’t hand over custody to the protocol and that trades settle on-chain.

These factors can all be true on the identical time. A regulator can keep away from saying a protocol is banned, and the protocol can proceed working as designed, whereas the warning nonetheless adjustments the general public body round who ought to use it, what protections customers have, and whether or not the interface creates the impression of regulated entry.

Hyperliquid’s documentation describes high-performance on-chain derivatives infrastructure and broad protection of perpetual markets. That’s central to its enchantment: it provides customers an expansive derivatives venue whereas routing the core settlement story via on-chain infrastructure.

The MAS itemizing assessments the a part of that mannequin that technical structure leaves open. A protocol may be permissionless on the settlement layer, whereas most customers nonetheless meet it via a web site, a person interface, documentation, social posts, market pages, and third-party discussions.

These layers create expectations earlier than a commerce ever settles.

Singapore’s public supplies deal with whether or not shoppers might imagine an entity is licensed or licensed, and MoneySense emphasizes what customers lose when dealing outdoors the regulated perimeter. For on-chain derivatives venues, that places stress on the presentation of entry as a lot as the supply of code.

The sensible questions are simple. Does the interface inform customers which jurisdictions it’s geared toward? Does it state what protections customers do not need? Does it stop or discourage entry the place the operator sees clear regulatory danger? Does the venue interact with regulators as its person base and market footprint develop?

Scale turns disclosure right into a stay take a look at

The market context makes the alert greater than a distinct segment compliance footnote. HYPE is at present a top-10 asset as of June 26, with roughly $15.7 billion in market capitalization, about $870 million in 24-hour buying and selling quantity, and powerful 90-day efficiency.

Regulator warnings hit in another way when the topic is a big, liquid venue moderately than a small experimental app. A retail person who sees a serious token, seen quantity, lively markets, and a cultured buying and selling expertise might infer a degree of market acceptance that differs from native authorization.

That’s the hole Singapore’s warning framework is constructed to handle. The framework asks whether or not shoppers would possibly wrongly perceive the standing of the entity they’re coping with and whether or not they perceive that MAS protections might not apply.

For Hyperliquid, the implications are reputational and operational earlier than they’re technical. The community can proceed settling trades, however the venture’s public posture might now face a better bar.

Clearer jurisdictional disclosures, entry messaging, and regulator-facing communications change into extra essential because the venue’s scale makes it tougher to argue that client notion sits outdoors the operator’s accountability.

The stress additionally lands at a second when Hyperliquid’s entry mannequin has already been beneath dialogue. A June 24 CryptoSlate article reported that Changpeng Zhao praised Hyperliquid’s no-KYC mannequin earlier than noting lawyer involvement as a sensible constraint.

Earlier in June, one other CryptoSlate article coated a UK warning that raised issues about unauthorized companies round Hyperliquid.

Hyperliquid’s case previews how giant on-chain derivatives venues could also be judged as they change into simpler for retail customers to search out and use.

The technical declare of permissionless infrastructure stays essential. Regulators can even deal with what customers are led to imagine about licensing, native protections, and who stands behind the interface when an app begins to resemble regulated market entry.

Potential subsequent indicators

Singapore has proven this distinction earlier than. In its 2022 statement after FTX’s collapse, MAS stated Binance had not been banned in Singapore, whereas additionally pointing to licensing and solicitation issues.

That precedent entails a unique reality sample, but it surely exhibits that MAS can separate a technical or sensible entry query from a licensing and warning-list query.

For DeFi derivatives, that separation is more likely to change into extra essential. A venue can defend self-custody and on-chain settlement whereas nonetheless needing a extra mature reply on jurisdictional availability, client warnings, front-end design, and regulator engagement.

The indicators to look at now are adjustments in how Hyperliquid and different giant on-chain buying and selling venues communicate to customers in particular markets. Potential responses may embrace clearer Singapore-facing disclosures, revised phrases, entry notices, geofencing selections, or direct regulator-facing constructions.

Any of these would present that the stress level has moved from the chain itself to the user-facing layer round it.

Till then, the MAS alert leaves DeFi with a extra uncomfortable message than a proper prohibition would have. Permissionless infrastructure can maintain working, whereas consumer-protection programs can nonetheless form how that infrastructure is offered, understood, and trusted.